Now that bitcoin is a mainstream asset, with futures contracts traded at the world's largest exchange, becoming actual money should be the logical next step. But if you were to ask investors their expectations, the reply in most cases would likely be: "Not in my lifetime."

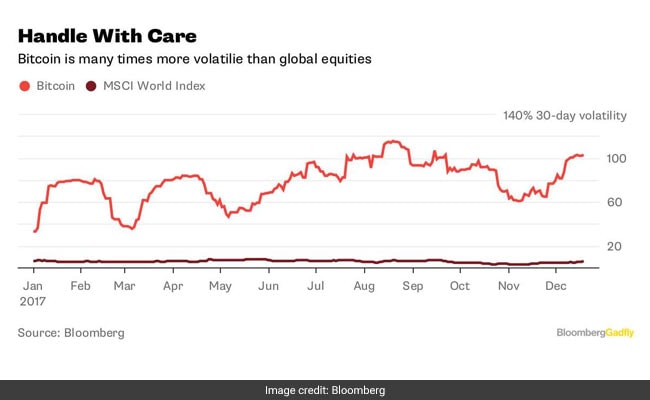

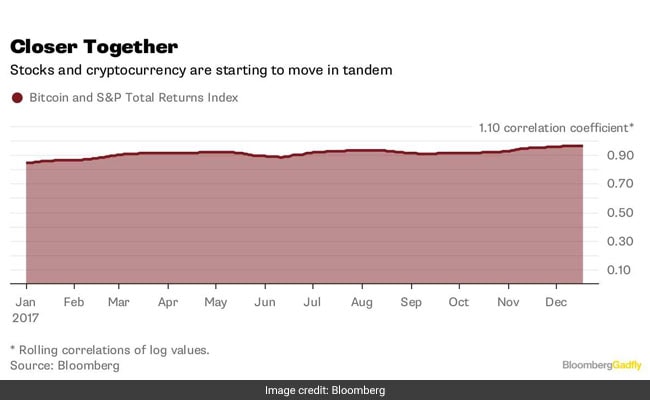

After all, even as an asset, the digital token's volatility is a damper. Researchers Pelham Smithers Associates and Albert Maass reckon that bitcoin is 25 times more volatile than stocks, and since it moves in lockstep with shares 94 percent of the time, only about 4 percent of an equity portfolio can be substituted without taking more risk for the same reward. So much for storing wealth.

Yet, too much pessimism may also be unwarranted. Bitcoin may only be suitable to replace 4 percent of an equity portfolio today. But the more widely it's traded, and the sooner investors have access to a fuller suite of derivatives, including options, the faster extreme opinions will dissipate. The anchoring of prices around more rational expectations would lower volatility, and lead to bigger portfolio weights.

Bitcoin is 25x more volatile than shares.

On the money side of things, progress may be messier. That's because throughout history, cash has been inseparable from the power to inflict violence. Notes and coins, issued by central banks, have value when they're backed by a strong state with the power to collect taxes and throw people in jail. But large internet firms and the government are now coming together to promote a new system of digital money and credit that is inseparable from identity -- or those parts of identity that people surrender when they add a social-media friend or use a digital wallet. In the new system, the threat of violence is implicit in damage to reputation in case of infractions; for good behavior, there are rewards.

As this article in Wired explains, this is already happening in China. India, too, is linking everything from pensions and bank accounts to meals for schoolkids and Amazon deliveries to a gigantic national biometric database, whose overreach has already spawned robust resistance. From an efficiency perspective, extreme centralization of data may be highly desirable for governments and businesses: Ant Financial, the payments affiliate of Alibaba Group Holding Ltd., has a winner in Sesame Credit, a scoring system that scours innumerable pieces of information to determine creditworthiness.

But if data analytics is allowing centralization, blockchain is enabling its opposite. As Bernstein analysts Gautam Chhugani and Gaurav Jangale note, there are those who believe customer's data should be owned by the customer and not by any intermediary. The more governments and businesses push for centralization, the stronger the backlash.

Microsoft Corp. and International Business Machines Corp., among others, are backing a decentralized self-sovereign identity, with individuals in control of their information, and sharing only as much as they need -- via tamper-proof, cryptographic statements of truth. When projects like these gain momentum, that's when bitcoin -- the first citizen of the decentralized economy, according to the Bernstein analysts -- will become an alternative currency.

But for it to be a significant, or even the world's, currency, banks will have to be stripped of their power to create money out of thin air by making loans. Otherwise, 21 million bitcoin, the maximum allowed under the current protocol, will be miserably inadequate during a liquidity crisis.

Lenders will resist a profit-sapping reshaping of the financial architecture until people's desire to own their own data becomes so strong they refuse to do business on any other terms.

The bitcoin community should thus hope that governments overplay their hands with experiments such as Chinese-style social scoring. It's probably the only way cryptocurrencies will live up to their full potential.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

(Andy Mukherjee is a Bloomberg Gadfly columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.)

Disclaimer: The opinions expressed within this article are the personal opinions of the author. The facts and opinions appearing in the article do not reflect the views of NDTV and NDTV does not assume any responsibility or liability for the same.