Prannoy Roy And Ruchir Sharma Discuss Top 10 Trends Of 2023

Ruchir Sharma, Founder of Breakout Capital and Chairman of Rockefeller International, lists out the top 10 things he feels will trend in 2023. In a discussion with NDTV's Dr Prannoy Roy, Mr Sharma talks about how the global and India's economy will behave after two years of Covid pandemic.

Here is the full transcript of the discussion:

NDTV: Hello and welcome to what I consider to be one of the most important shows that we've been doing for several years now and will continue to do so in the future. I must admit but don't tell Ruchir this, Ruchir how many years has it been?

Ruchir Sharma: It has nearly been a decade since we've done this show, but obviously we've been on television a lot longer.

NDTV: Right, I must admit and I was saying that I don't want Ruchir to hear this, that I learn more from this regular interaction with Ruchir Sharma than from almost any other programme that I've done. I must update you very quickly that Ruchir has now set up his own organization which is called Breakout Capital which is already doing brilliantly, has only recently started, so just watch this space.

Don't blush now Ruchir, I can see. I must point out like I do every year - all the research and analysis for this programme is done by Ruchir and his fantastic team and as you know it really is amazing research. Once again we should look at 10 major forecasts for this year, 2023. Let's first spend a few minutes understanding what actually happened last year and Ruchir your earlier forecast for 2022, shall we go through that - the 10 forecasts that you did get last year.

Ruchir Sharma: Yes, yes that's usually the routine.

NDTV: Okay, so let's look at the first forecast that Ruchir made in 2022 last year. Here it is. He said there'll be a decline in the birth rate and that will accelerate. In actual fact they didn't accelerate, birth rates stabilized a bit. There was a decline but they stabilized. The rate of decline in the world flattened a bit and India is also flattening a bit. Why that changed do you think?

Ruchir Sharma: You know I think what happened during the pandemic they got a major drop off in the birth rates of many people, but last year in 2022 in terms of the birth rates had been declining as you can see from the graph, the birth rates around the world have been declining dramatically really for the last few decades, and that pace has been accelerating in the last few years, did so even more during the pandemic. But in 2022 we saw a bit of a bounce back where the birth rates increased in some of the countries, possibly as a catch-up to what happened in 2020 and 2021. But the long-term trend I think still remains intact. Which is that the world is seeing a decline in the birth rates and therefore the population increases around the world have also being slowing down very sharply.

NDTV: And you pointed that related to a smaller workforce and that could affect growth rates of the economy.

Ruchir Sharma: Yes, and that's an affect that we are seeing around the world. Growth rates, the potential growth rate of the global economy due to declining birth rate and deteriorating demographics is falling everywhere. So the global economy which used to grow at let's say at 3.5, 4% now is lucky to grow at 2.5, 3% largely because of the demographic changes.

NDTV: I mean this is an amazing finding and I don't think many people, I don't think anybody else really related the two and then they just copied you. Let's look at the second forecast that Ruchir made last year. He said that China's economic power was peaking and actual fact, yes, China's economic power has peaked. if you look at the growth rate, look at it compared to the rest of the world, it was 10.3 compared to the rest of the world's 3.8. Back in 2000s about what, 7% above global, then it was about 5 to 4% above global and now China and the rest of the world's growth rates are about the same. So that rapid development compared to the rest of the world has seemed to have gone recently.

Ruchir Sharma: Yes so, that's my point, we are at that moment now where China, the best economic growth rates are well behind it, it is a middle-income country, it's facing all sorts of challenges. We spoke about demographics at the outset of the show. Very few developing countries have a demographic profile as bad as what China has because of its one child policy having such a lagged impact now. Its debt levels are very high. The property sector is really saddled with too much debt. And so therefore my forecast is also that in the coming decade China's growth rate is likely to be closer to 2.5% on average.

NDTV: That's a huge change.

Ruchir Sharma: Right and we only saw that in 2022 that China's growth rates fell a lot. Some of it I think was suppressed because of its zero Covid policy which had been a failure and now it's reversing course rather dramatically on that. So, China's growth rate might bounce back in 2023 but the long-term forecast based on demographics, debt and productivity is that China's economic growth rate is unlikely to be faster than that of the global economies. So, China's share in the global economy may have also peaked and that is a huge development because no country gained as much share in the global economy as China did in the last 4 decades. It was a dramatic rise.

NDTV: So dramatic I mean. As you showed growing at 10% on average for a few decades, it's just phenomenal and that's gone. I'm a bit surprised it hasn't gone up base effect because after the pandemic you think the next year there's a low base. The growth rate will be higher, but even that hasn't happened.

Ruchir Sharma: That may happen in 2023.

NDTV: Just because of the low base effect?

Ruchir Sharma: Yes because they were the last people to exit the zero Covid strategy, so that suppressed growth. So that may happen in 2023 but we're more interested what the long term trend growth rate in China is and I think it's two and a half percent a year, which means that it's unlikely to grow faster than the global economy for the foreseeable future.

NDTV: Ten percent to two and a half percent - that is just a phenomenal change. Let's move on to the next focus that Ruchir made last year. He said that the global debt trap will deepen, in actual fact, yes, mostly it did. But India was stable, the debt servicing cost of the share of income, if you look at the world, is rising, debt servicing rising India not rising, in fact falling a little bit if not stable. That's a big difference between India and the rest of the world.

Ruchir Sharma: Yes, this is mainly for the private sector, so I think that in India's case the private sector has the leverage. They have reduced the debt burden and so therefore they are in a better shape just now but around the world particularly in developed countries, in places like the US, they had taken on so much debt on the private sector side in terms of the firms, that as interest rates have gone up, the cost of servicing the debt has been going up a lot, so therefore the forecast last year that the debt gap deepens and it seems to have played out that way.

NDTV: Yes, that is a worry actually because implications for the future. Moving onto the next forecast that Ruchir made last year, this was that inflation will rise but may not hit double digits, that's quite a bold forecast and actually yes, it only increased to 8.8, it didn't hit double digits. Of course it did rise as Ruchir had forecast and it's kind of back to the levels of the 80's but didn't hit double digits, not terrible but still worrying because 8.8 is high.

Ruchir Sharma: I think a lot of people at the beginning of 2022 when we did this show were looking for inflation to rise. Some were looking for it to rise explosively. Others thought it would be transitory. I think we got something in the middle, that yes inflation did rise, but now it seems to have peaked, which is that across the world the inflation rates look to have peaked. But as we discuss in the show subsequently that it's likely to remain much higher than where it was in, let's say, in the 1990's or the 2000 so higher and stickier inflation but not the 1970s show where inflation was in double digits for a long period of time.

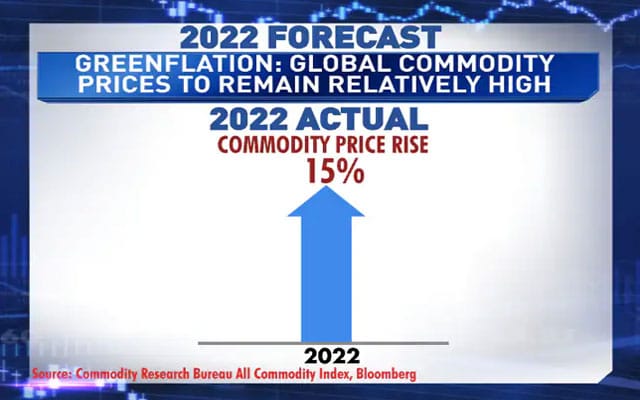

NDTV: Yes, that is a significant difference. The next forecast that Ruchir made last year was about greenflation that's about commodities and the commodity prices going up. He had forecast that global commodity prices in 2022 to remain relatively high, in fact commodity prices did remain high, in fact they went up fifteen percent. That is relatively high compared to other prices. Why is that still happening?

Ruchir Sharma: Yes that's a pretty significant outperformance because remember most assets like stocks and bonds around the world have fallen significantly in 2022. The reason that commodity prices have been more resilient has been because of oil, energy partly driven by what happened in Ukraine, but I think it's much deeper than that, which is that because of concerns about the green environment, you've had a lot of supply cuts, that not much new capacity is coming for commodities because people are very concerned about the impact it has on the environment and lots of regulations and political pressure is their dissuading people from...

NDTV: So, in a way there's a positive aspect of that - people are being more careful about how they mine, how they destroy the environment.

Ruchir Sharma: Yes but the negative effect is that fact that you are getting high commodity prices. So how do you get from point A to B remains a challenge. We all want to greener environment, but the problem is to build a greener environment it takes time A and 2 that it also requires some of the commodities to build the new green infrastructure, whether it's copper or aluminium, some of these so called dirty metals you need them to build the infrastructure.

NDTV: To improve the environment, it's a tough one ahead.

Ruchir Sharma: It's a tough one. But supply has been constrained and demand has been weak but because supplies been so constrained this time that even in a global slowdown, commodity prices had been relatively resilient led by the energy complex.

NDTV: Right. Moving onto the next forecast that Ruchir made last year and that was that productivity paradox persists, low productivity, there will be low productivity. Yes, in fact in actual practice, productivity remained low despite the tech boom. A lot of people said technology is going to change the world and you know productivity is going to go shooting up but we just see from his graph, that in 2021 there was a kind of post pandemic flare up because of unproductivity, partly because of the tech boom but then it's gone back again. There is low productivity now so the tech boom Ruchir has not improved productivity, it's a shocker.

Ruchir Sharma: Yes, there are many reasons for this. Some of the reasons that I've written about is that it could be that you have so many zombie companies out there, so many inefficient companies being artificially propped or were artificially propped by very low interest rates, too much stimulus, so that's been eating away at the creative destruction fabric of economy, so the explosion. And zombie companies, too much government intervention have been keeping many inefficient companies alive - that could be one reason for this.

The other reason, some people say, that the kind of technology we're seeing, whether it's gaming, or other things, are more distracting than enhancing as far as productivity is concerned. So I think this is a very deep research topic which is that why in the midst of the tech boom do productively numbers continue to look so poor. I think a good reason for that could be the fact that you have too many inefficient zombie companies which are kept alive. One statistic like in the US, the number of inefficient zombie companies, companies that are not able to even service their debt without borrowing more and more that, that number too shot up from nearly two percent in the 1980's to nearly twenty percent now.

NDTV: So 10 times, zombie companies have gone up ten times.

Ruchir Sharma: Yep that's right and that could be chipping away at the creative destruction fabric of any capitalist economy.

NDTV: I know none of our viewers would like to hear this but has this low productivity got anything to doing do with working from home. I mean a lot of, I mean the pandemic is sort of temporarily over, but people still want to work from home?

Ruchir Sharma: It depends on who you ask and that extra shows.

NDTV: Depends on what you actually believe. The next forecasts he said did working from home help or hurt productivity. Employees or staff say they are productive at home, let me stay at home I'm as productive, eighty seven percent say they are productive at home but their bosses say, sorry I don't believe you. Only 12 percent of bosses believe that employees are productive at home, so what's the truth?

Ruchir Sharma: Like I said it depends who you asked. If it's clearly not showing up in the productivity numbers so maybe the bosses are a bit more correct, we don't know or it's too complicated a model, but I find this fascinating about this dichotomy in terms of what the employees believe and what the bosses believe.

NDTV: But I think your productivity won't go down because you've always worked from home.

Ruchir Sharma: I wish that was the case

NDTV: Let's move on to the next one, amazing, bosses versus the belief of bosses they live in another world these bosses. Okay let's have a look at what Ruchir forecast in 2022 - that they'll be increasing data localization and that actually what happened is data localization in 2022 did intensify. Look at Russia, it's kind of weaponizing data localization. Maybe you could run us through China racing to block global dissent, US senators want to stop TikTok, India already did. And this is a bit shocking, from your data India is 5th worst in the world in terms of data restrictions. We just come after China, Saudi, Russia, Indonesia and then India in terms of data localization.

Ruchir Sharma: Yes this is an index which is maintained by the OECD, which looks like in terms of what has been the digital services enabled businesses and of what sort of barriers and data restrictions they face. So that's what the OECD ranking is, so it is what it is. I think that there are about 80 countries in that ranking, of about 45 emerging markets in that ranking and so that's where India's ranking is as per that. I'm hoping that improves if you have a new, I'm told, a new draft privacy bill which may help improve that, but as of now that's the case and around the world we have seen that there's been much more of an effort to keep data within countries and not allow for it to really go beyond borders and that something which is...

NDTV: Why is everybody so worried about TikTok? I mean the US wanting to ban TikTok.

Ruchir Sharma: I think it's pretty obvious it's Chinese and so popular and I think that they have very sophisticated algorithm, AI systems, which I think a lot of people feel sort of breaches the line.

NDTV: Kind of swoop into people's private lives etc, yes, right. Next one this was amazing - Bubblets deflate, that means that a lot of small little parts of the economy that are doing very well and you said they're going to deflate or they were doing brilliantly and now look what actually happened. They did fall, further they did deflate. Bitcoin, of course, we all know gets the most publicity, down 64%, tech companies with no earnings. Some of them are zombies down 53%, SPAC down 41, Green Energy down 25, huge change there - those are big figures.

Ruchir Sharma: Yeah in 2021 I had identified a few Bubblets, you know which are really about good ideas gone too far in a way. Which is that these were good ideas but got too much speculative interest in them and so I identified them as Bubblets and I said that typically if you look at the path, Bubblets tend to fall by 70% once they peak and I think that we have roughly seen...

NDTV: Yes, look at that, I mean it really is...

Ruchir Sharma: This is just for the year, from the peak they are down even more because some of them started declining in 2021, this is for the last year's, they, yes they have 2022

NDTV: Averaging fifty, it would be at least 70%

Ruchir Sharma: Yes mostly these Bubblets have deflated by 70% percent so that sort of played out from the peak.

NDTV: The next let's have a look at the forecast Ruchir made in 2022 said small investors mania for the stock market will cool down, in fact in practice in 2022 actually what happened was lower investment by small retail investors happened in India. Look at India's retail flow, that means retail investors, how much they did they invest in shares, dramatic decline in this one year. It is quite a serious, from fifteen hundred to five hundred is like a huge fall yes, one, and why are retail investors losing interest?

Ruchir Sharma: It's partially because we saw such a massive inflow in 2021 that is cooling off now and the other thing of course is because interest rates are going up in India, so now all of a sudden people think that by putting money in the bank accounts or fixed deposit to be able to earn some return, so therefore the very negative interest rates you had in India. have changed now and so therefore the, like retail mania cool, then again it's happened around the world that in the US for example we've seen a massive cooling off of retail mania. In fact there we see big out flows with people pulling money out of US stocks and bonds because there in the US obviously the markets are down a lot more than in India, so the markets cooled off a bit around the world including in India, although India's much better than US but in general the retail mania around the world has cooled.

NDTV: So is this something that the big investors know, that the retail investor because the big investors are still investing in the market with the retailers or the asymmetric information the as usual poor small investors are getting don't know something which the big guys know?

Ruchir Sharma: Well, I'm not sure but I think the general they got too caught up in the post pandemic boom euphoria you know. I think that's sort of cooling off now, right.

NDTV: One more forecast let's have a look at the Ruchir's focus for 2022 that the physical world is still more important than the virtual world and Metaverse. In fact what happened and 2022 the physical world investment was actually as he said much higher than the new virtually economy. Look at the last ten years before last year, the investment in new economy was up 5% and in the all the economy down 7% that's a twelve percent difference. Advantage 12% for the new economy. In 2022 the new economy grew by 5.7% and the old economy 9.7%, from minus 7 to 9.7 that's a 16% swing. How did you figure this one out?

Ruchir Sharma: Well the world had under invested a lot in the traditional physical economy, whether that it's, we spoke about commodities and the underinvestment due to the green politics and then even in machinery, equipment, industrial, they are under investing because everybody was so focused on investing just in tech. So as the tech bubble has burst, I think that people at once again gone back to focus on the old economy and how we need much more of that basic infrastructure to still function and those shortages came true and that's a reason why inflation flared up as well because of the under investment in the physical economy.

NDTV: Well that was the last of the ten forecast that Ruchir made in 2022 and I hate to say this to your face Ruchir and don't blush, you got 90% right and even the 10, one that you got wrong out of 10, that was pretty close to getting it right as well. This the downward trend but is still flattening so I give you 97%.

Ruchir Sharma: The past has no prologue so now we are going to see what happens.

NDTV: Now comes the real thing. We move on to what's going to happen in 2023 was going to happen to this this year ahead and what are Ruchir's forecasts for that and remember 97% right in 2022 last year and now, now 100% right. Okay the first thing you're forecasting is there's got to be a long grind, by long grind you mean there's going to be no bust and no boom. It's not going to be a dramatic recession. You're saying they're shorter recessions now because of easy money, higher government spending and low interest rates and if you look at the shorter recessions according to Ruchir in pre-World War 2 the percentage of time that there were recessions was forty four percent, nearly half the time economy was in a recession, then from World War 2 to 1979 almost twenty percent, nine, eighteen percent of the time was in recession. That's high now because of all this easy money era, it's down to half that and one fourth of what it was. This is a huge change.

Ruchir Sharma: Yes, I think that this has a lot to do with the role of government stimulus, government intervention. That in the pre-war era there was very little of government intervention, economies such as the United States or the developed economies of that era right and it's really since then that you've seen much more government intervention and specially in the last three four decades, as inflation was declining, every time there was the slightest trouble. Because inflation was low and falling the governments and central banks were able to come out there and put out a lot of stimulus and that was particularly true in the pandemic that we saw stimulus like never before during the pandemic.

NDTV: Its amazing data, forty four to ten percent so you're saying John Maynard Keynes was right?

Ruchir Sharma: In terms of, I'm not sure right or wrong, but he clearly had the maximum influence on policymakers and generally on economists

Prannoy Roy: And as you are saying your data shows that in this long grind ahead government stimulus or rescues increased sharply leading to shorter and fewer recessions. Look at your data on stimulus as a percentage of GDP, used to be 1% in 1990, right now it's 46% this time. Amazing change.

Ruchir Sharma: Yes but the only downside of this is it going to be made earlier then because it's so much stimulus, so much intervention, are we keeping too many inefficient companies alive? Are we not allowing the natural process to play itself out where a lot of zombie companies that are deadwood gets cleaned from the system, so that's the downside. But the long grind that I'm forecasting now refers to something a bit different. Which the issue is that we being in this era now, as Isaid that as you had declining inflation and you kept getting lower and lower interest rates and the government's what's able to stimulate and also cut short recessions, the problem now is that inflation I think is likely to remain stickier, inflation has peaked and is coming off in many parts of the world. But the 2% inflation that we had for much of the developed world are as likely to be more like 4%. Why? Because the demographics have shifted, the people's attitude towards work has shifted, so even now if you look at it the global economy has been slowing down and yet unemployment rates around the world are close to record lows, so it's very hard to get people to come back into the labour force. A lot of people are still living off a lot of the stimulus that was put doing the pandemic. In fact some research shows that nearly half of that excess savings that people built up because of the massive stimulus following the pandemic is still sitting in people's bank accounts, so you know, like the whole idea being that that provides a cushion, so the problem is that it delays inevitable which is that you have so much monetary tightening and yet the global economy has been relatively resilient so far, but the problem is that once those savings run out and then the recovery time starts, the recovery may also be soft and the shape may look like a long smile rather than...

NDTV: Kind of a V, exactly the normal the old recessions used to be a sharp down and a quick sharp up now you're saying it is going to be a long grind, kind of a not a V anymore?

Ruchir Sharma: Yes and that's because inflation is likely to be stickier and because of stickier inflation the capacity of governments and central banks to stimulate will be much more limited, so therefore I feel that we're in this period of the long grind. NDTV: Finally, just wanted to look at your data on this long grind and what are the implications for India and the quite important very, very, serious actually, because as the world slows so will India slow down, because historically India's growth rate according to all Ruchir and his team's data, India has been only slightly above the world in terms of growth rate. So, if the world slows down India's growth rate is unlikely to be above 5%. Historically India's growth rate has been above the rest. Look at the world on average has been 3.4% growth rate, India has been 6.1, so has 2.7% above the world and compared to emerging markets India has been 1.4% higher than the growth rate. Now explain what happens if there's this long grind, what are we looking at?

Ruchir Sharma: The point I'm trying to make here is that we under estimate systematically, this is a debate I've had with so many people in India. We under estimate the global linkages. India's growth rate is very tied to what happens to the rest of the world, at least at the margin there's a 70% correlation between India's growth rate and the rest of the world's growth rate and the point is that it is very difficult for the Indian economy and it is historically so, to grow that much faster than the global economy. It's quite significant that we have grown nearly three points faster than the global economy, but it's impossible to sustain a growth rate much above. That is what we have seen even during the boom years of the 2000's. Compared to the developed markets and even other emerging markets India's growth rate was capped beyond a point. So, I think that if the global economy slows down in 2023 as we forecast to about 2% or so, that India's growth rate is likely to be closer to 5% based on this historical fact pattern.

NDTV: Does it really gets capped? I mean even three percent higher than the rest of the world is pretty high, but if the rest of the world slowing it really slows down India.

Ruchir Sharma: Yes and the problem here is if we make our forecasts quite insulated from that, we keep talking about six percent, seven percent, eight percent, those growth rates were possible in the 2000's, but a time in the global economy is going to grow at two percent, then for us to grow much of a five percent is going to be nearly impossible until something very dramatic China-like happens...

NDTV: That's really fascinating and one has to take this into account and in all policy decisions that is five percent now and how do we tackle that in the economy?

Ruchir Sharma: Right

NDTV: Now the dollar has been rising, rising compared to all other currencies but you're saying the seeing the peak of the dollar. If you look at Ruchir's data this what it looks like. Every time the dollar rises it's followed by a downturn. Look at those three and you're now hitting eleven years which is much longer than peaks that dollar's taken to reach eleven years has taken and so you're saying we're going to have a downturn now, the dollar which means the Rupee will strengthen in comparison, all other currencies

Ruchir Sharma: Yes I think that the, you know, in terms of the well the Rupee has weakened significantly against the dollar over the last seventy five years as we last spoke about it. But the Rupee's depreciation against the dollar has been particularly sharp over the last couple of years and I think that that's likely to slow down.

Because the dollar in general is looking very expensive against major currencies around the world. Now this is a very important graph in some way that the dollar is the world's reserve currency, but it doesn't always rise, the dollar spends time going down, it spends time going up, it fluctuates against the major currencies.

NDTV: Fascinating graphic. Actually yes.

Ruchir Sharma: And I think that the dollar has spent a long time going up over the last decade but typically after rises so much and it feels so expensive the dollar spends the next few years declining, so I anticipate that the dollars has peaked against most major currencies such as the Euro, such as the Yen. And that in the next few years it's likely to decline against those currencies. Also because the US now is running very large deficits, it owes a lot of debt to the rest of the world and also what happened I think last year in 2022 into was very significant that the US used the dollar as a weapon to impose sanctions against Russia, but what that's done is that many countries around the world including India looking at ways how do they reduce their reliance on the dollar, how do they trade with other currencies and other countries in their own currency rather than trade so much against with the dollar as the invoice currency, so these are changes structural...

NDTV: Very crucial for policymakers to hear that. Okay. You're saying there's a long-term decline of the Rupee against the dollar but it was very sharp decline in the last two years, while it might continue to be a decline in won't be as sharp as the last two years

Ruchir Sharma: Yes I think that's the finding and that it's backed by the fact that it feels very expensive as this graphic shows.

NDTV: Amazing actually that you've looked at that because of this expensive dollar the US cities have become the most expensive cities in the world. The rising dollar you're saying is a major cause. In fact in the ten most expensive cities New York, where you live, New York City is the world's most expensive along with Singapore, then there's Tel Aviv, Hong Kong and then Los Angeles; that's dollars, Zurich, Geneva, traditionally expensive, San Francisco, again the dollar and then Paris and Copenhagen and Sydney. So, the dollar's made cities in America expensive. How you do you manage?

Ruchir Sharma: Yes so. I've been in New York for twenty years. It's never felt that expensive and it's backed by this data and in fact I don't I can't think in my memory when New York was the most expensive city in the world. And that's what's happened out here. So that tells you further that a dollar has become very overvalued, very expensive and is likely headed for some sort of a correction.

NDTV: Right, this is almost like burger. When burgers get too expensive...

Ruchir Sharma: The Burger Index you know like or even the hotel price rates.

NDTV: The cities are more interesting because that's what people experience

Ruchir Sharma: Yes that's right.

NDTV: So nobody should go to New York right now. That's what you're saying deep down. Okay in this peak dollar forecast Indian cities are becoming the cheapest in the world. Three out of the top ten cheapest cities or bottom ten cheapest cities are in India, the world's least expensive cities and those are Bangalore, Chennai, Ahmedabad and then you can see all the rest on that list and these are world rank 161 down to 172 cities So everybody should come to India.

Ruchir Sharma: This is a survey done by The Economist intelligence unit. They do this. I think on an annual basis and yes, it's a telling sign, these are many indications of where the dollar is. It's a telling sign that some of the most expensive cities in the world are in America and some of the most cheapest cities in the world are in developing economies, which they always are, but the fact that India has 3 out of those ten spots is interesting.

NDTV: Amazing. On the next forecast you say that when America goes down, which it will, the rest of the world will rise. The data from that is actually also fascinating. America down, rest of the world rises. First of all America down and the rest of the world up because US stock market values are disproportionately high, I never realised that. It's got 4 percent of the population and is punching well above its weight. It's got 4 percent of the population and 60 percent of the market cap. That is just out of whack. And 25 percent of GDP. And still that's the economy and 60 percent of the stock market capitalization.

Ruchir Sharma: Yes, America has always had the most dominant and best-performing stock market in the world. Over a very long period of time, if you look at the last hundred years or so, America has been at the top of the charts, it truly has a true capitalist system that way, but what's happened in the last decade is extraordinary, which is that the American stock market has done so well, has outperformed all of the global stock markets by such a massive amount that we now have a situation where, despite the fact that America is only twenty-five percent of the global economy, that share has remained stable for a while now, America's share of global stock market values is sixty percent and that's never happened before...

NDTV: Has this ever happened before?

Ruchir Sharma: Yes

NDTV: Wow.

Ruchir Sharma: That number has been closer to forty to forty-five percent, because America has always had the most dominant stock market in the world, but at sixty percent, that number is way out of whack, and I think that number is also bound to correct itself in the next few years.

NDTV: Ruchir, another fascinating point you make is that America is like a seesaw, when America is down, the rest of the world is up, America goes up and down after each big decade, America has a downward decade, if it goes upward one decade, it goes downward the next, compared to the rest of the world. For example, look at this graphic, America versus the rest of the world. It was going ten points one percent higher than the rest of the world, and then next decade minus three point three lower than the rest of the world, then up seven points six, so what do you make of that now? You're saying it's going to go down.

Ruchir Sharma: Yes, as I said, if we look at the hundred-year history, then the American stock market has been the best-performing large market by a long shot. But it follows this pattern: after it does very well for one decade, especially the recent 4-5 decades we've seen, in the subsequent decade, the American stock market tends to underperform the rest of the world, because it becomes too expensive and expectations become too high. So after this very extraordinary decade that America has had of great performance I think that it is now set for underperforming in the coming decade, also because its size has become disproportionate, so that will allow other countries, including emerging markets such as India, to do much better than America. That's my forecast, and I think in 2023 we are likely to see shades of that play itself out.

NDTV: Already, funds are moving out of America because they think it has peaked in comparison to the rest of the world, and other stock markets may improve.

Ruchir Sharma: Just about, in the last few weeks and months, we have seen some signs of that, but this is a very long-term process; it takes a while because most people are still anchored to the past; they still look at past returns and feel, "Oh, why should I go anywhere else when America has done so well?" But the point here is that these follow these decadal rhythms that we are likely to shift in 2023 onwards, towards the rest of the world doing much better than America.

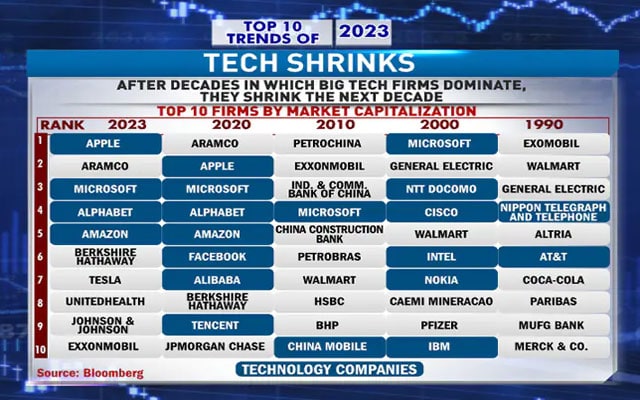

NDTV: Very interesting. The other point you make in your next forecast is that tech stocks are going to shrink, and if you look at that, that's what happened after decades in which big tech firms dominated; they shrank in the next decade. That's historically true. These are the top ten firms by market capitalization. If you're in the top ten one decade, there is a high probability that you will not be in the top ten the next decade, just ten years, and you can transform everything.

Ruchir Sharma: Yes, so I think that this is very telling, that by market value, the top ten firms in the world at the beginning of every decade change, and as you can see, eight to nine of them change. And when we had the last tech boom, which ended in 2000, the top tech firms in the world then were very different from what you have today; those days you had Cisco, Intel, and IBM. The only survivor in a way has been Microsoft.

NDTV: Microsoft has an amazing track record.

Ruchir Sharma: Yes, but the top tech firms in the world today are very different from what they were back then, as you can see in the last 2 or 3 years there has already been a lot of churn that has been taking place. The Chinese tech firms have fallen off, they are no longer in the top ten. Even in America, a firm like Meta, Facebook's parent, that used to be in the top 10 is now not even in the top 25. So this churn has begun and I've been telling people that I will not allocate any money or capital to these tech firms because that's the nature of the game, that once you become so big, so dominant your business model gets spent, more competition comes in regulatory pressure increases and that sows the seeds for new firms to emerge. And in general I feel that tech space became very over valued and overheated, and that's going to cool down and we're seeing that effect in even India now where a lot of the tech craze that we had for some of the unicorns and other companies and that's cooling off.

NDTV: Yes. That's your next graph, that tech slowdown will hit India as well, and it has already, in 2021, 35% of all capital raised through IPOs were tech, and in 2022, it was 2%, so do you think this pattern is going to continue?

Ruchir Sharma: Yes, I think this was a climax we had in 2021, so in many ways for people who have lived through it, there are shades of this of what happened in 2001 or so with the big tech boom and then you had a bit of a bust, and even though technology is here to stay to be there for a long period of time, it will take a while now for this recovery to happen, for people to digest this mini bust that's happening. It'll be much more pronounced in the US but even in India you'll see some of that happening. Somenof that is already here.

NDTV: And I did want to censor this next forecast of yours, because you're saying more money for TV doesn't mean better TV and less money for TV means better TV. Just have a look at this data and don't take this seriously; TV needs money; in fact, less money has meant better TV, and money spent on TV content has surged from 2018 to 2014 from 89 billion to a hundred and forty-two billion, but the content has not done well. Just look at his data on content; this is the ratings of content and shows; it's just a downward slide, and more money is spent, and it's just going so less money could mean better, and that's what's happening.

Ruchir Sharma: I think that's what could happen. The basic point is this, this has been the golden age of television as you know, especially for streaming. We saw a surge in the number of new streaming services, and we saw so much cheap money available to fund new projects and new series so global content spent on television surged over the last few years. But my point is that quality went down. That so many shows were commissioned which were possibly poorly conceived with the script or the concept was improperly done, but just in a hurry to get new subscribers, new users we got so much content out there that the quality went down, the focus was on quantity, and now what's happened is that as you get much tighter money in general, as we've argued because of higher interest rates.

NDTV: They will sort of raise their bar.

Ruchir Sharma: Also, and also because the tech sector, which is the funder for a lot of this stuff, has gone bust, I think what happens now is that the focus on quality goes up because a lot less number of series get commissioned, a lot less number of shows get commissioned, and I think that this has as always implications for India, which we've already seen. That in India if you look at it what has happened is that a lot of these major streaming services, the Netflix, Amazon's, Disney, they had so much money to spend, they spent on buying all sorts of movies and buying lots of series and a lot of that was junk, was drivel in terms of that. But they sustained that by doing that, now they are cutting back dramatically.

NDTV: Even in India and in the world?

Ruchir Sharma: Yes, I've heard that some of India's leading services, if they were to buy, say, 30 or 25 to 30 movies directly to go digital, that number is likely to be in the single digits, maybe 6 or 7.

NDTV: From 25 to 6 or 7. Wow, that's a huge drop.

Ruchir Sharma: So that means the pressure on budgets and the stars' ability to charge is going to go down a lot.

NDTV: In fact, your graphic shows that's a global phenomenon as well, because they made massive losses, and after those losses, there have been major cutbacks on series being commissioned. Just look at the losses that were made by these streaming companies. 5 billion dollars in losses, and the reaction was to cut back on the number of new shows from 200 to 150 between 2021 and 2022, and you see that trend continuing.

Ruchir Sharma: Yes, that's for the US. We have this data that we will see the same effect out here, and I think it may be for the better if you could focus on the quality because today, when we were having these year-end dinners, when you go around the table and you ask people what were their favourite series of the year, people would struggle to come up with names. There's so much content out there, whether you try and come up with what were your favourite series or movies, very few roll off your tongue, so I think that because so much of it was just not well-conceived, and so much of it was just not well-conceived, that now we're more likely to have a stricter budget and possibly better quality going forward.

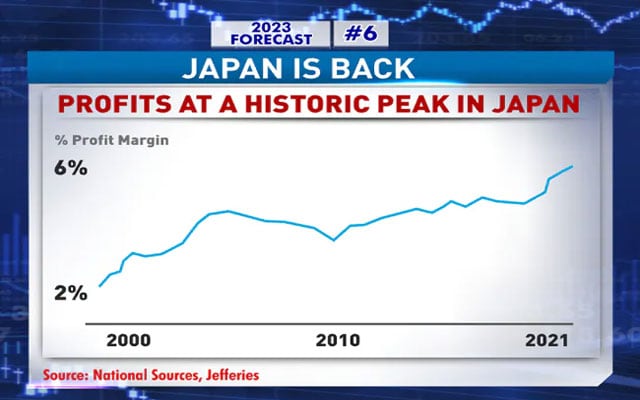

NDTV: So, you're saying less money for television? Fine, we'll cut that out in the final, when we put this on the air. Okay, the next point you make is that after decades of being a big worry in the world, Japan, with high debt and all that, Japan is back. That's excellent news, and you said earlier that Japan had a major problem with debt, and now you're saying Japan's debt is now better than that of other developed countries. For example, in the early 1990s, Japan's debt was many times higher as a percentage of GDP than the debt of developed markets. Now developed markets' debt is higher than Japan's. I think this is a transformation that is really welcome because Japan really did suffer for many years.

Ruchir Sharma: For many decades.

NDTV: Many decades of regret.

Ruchir Sharma: As you may recall, that in the late 1980s Japan was the shining star, accounting for 16 percent of the global economy and 45 percent of global stock market value. because of the bust that happened and the way it was handled, but also driven by poor demographics, with the population shrinking, debt levels so high, and other issues, the Japanese economy and the Japanese market have done very poorly for the last three decades. My point is that now quietly Japan may be making a comeback, because a lot of the problems that Japan has the rest of the world also has in terms, the debt levels have gone up, the demographics in the rest of the world; we're seeing more than 60 countries today have their working age population that is shrinking. That number when Japan first went bust in 1990 was barely 20 countries had a shrinking working age population. So the rest of the world has a way converging with Japanese standards...

NDTV: We're catching up to Japan, and Japan is ahead of us.

Ruchir Sharma: Japan is improving; its corporate profitability is improving over time.

NDTV: Yes, that's your next graph; look at it and explain to us how profits in Japan, which are now at a historic high, you know, a 2% profit margin, have increased threefold; that's huge.

Ruchir Sharma: Around the world we're seeing an increase in corporate profit margins, but for a country that was criticised for not focusing on profitability, I think it's interesting in Japan too that we're seeing this focus come through. And also some other points we discussed, like female labour force participation in Japan is very high, at about 85 percent, and you need more of that to try and offset the demographic disadvantage that Japan has and other countries too have. So it's a quiet comeback, it's not something which is headlined out there but I suspect this year in 2023 we're likely to see Japan do relatively well because of the fact that on the downside the rest of the world has converged with it; on the upside Japan has seen some major improvement from its corporate profitability to the female participation in its labour force, that should help Japan in general.

NDTV: Female participation has increased in Japan, and there is a lot of data that shows that female participation in India is very low, but that goes against reality when you see it. You see a man sitting and doing nothing, and the women in his family are picking wood, burning, getting water from a well, cooking, I mean they are participating, they are working much harder than the men who just don't get paid for it in India, so the data doesn't show their particpiation...

Ruchir Sharma: That is possible. Sir

NDTV: ...paying for their and one interesting point you bring up is that with Japan returning to and rising, it could lift India; foreign investment from Japan to India could go up from 3% to 7% and higher, that's the trend.

Ruchir Sharma: So, Japan's been a major investment partner of India. Having a healthier Japan with better corporate balance sheets could further that process. Even Indo-Japanese trade has slowed down a lot in terms of that. If you look at the exports that India does to Japan, Japan's become a less and less significant partner on that. But the Japanese economy does better, which could help our exports too at the margin. But the most important point is that Japan has been quite significant as an investment partner of India.

NDTV: Japan is improving, and the better Japan does the more India benefits.

Ruchir Sharma: Yes, that's correct.

NDTV: That's huge, and that is very good news for India. Your next point is about people no longer outsourcing to China but instead outsourcing outside China, and that could be a big opportunity for countries in Asia, etcetera. If you look at outsourcing to China from America, China's loses share of US imports has gone down by about 4%, while the rest of Asia has gained. India has only made a small gain, so China also seems to have gone down 4%. Other countries excluding China in Asia have gone up 4%. So far, India's outsourcing has increased by only 0.2%, why is it that we are not getting more of that change?

Ruchir Sharma: Well, first, to put this in context, for much of the last two or three decades, China was the factory of the world, where everyone in America or Europe wanted to set up a factory in China given the scale they have and the low wages they've had. The last few years a couple of things have happened: one, Chinese wages have shot up a lot, making it a bit more uncompetitive, and two, for geopolitical reasons, I think that people don't want to put all their eggs in the Chinese basket, they want to diversify out and so they look for new investment destinations. But very interesting they still want to outsource because the wages are still so much cheaper in the rest of the world.

NDTV: You are aware of this reality? Ruchir Sharma: Because wages in the manufacturing sector in America are over $5000 per month, but wages in the rest of Asia are not even $500 per month, so there is a lot of incentive to still outsource, it's just that people don't want to do it to China anymore.

NDTV: Because of geopolitical wages?

Ruchir Sharma: Wages are going up, and so which are the places that they are looking for? It's been Vietnam and Cambodia. Bangladesh's and even India's wages are very competitive, and we've seen some gains.

NDTV: Your data has that actually if you could take us through this because China wages are now much higher than the rest of Asia and you can see there is a wage advantage over China, which means we have lower wages than China and that is attractive for foreign investment and you can see India's you know way below China in terms of wages so it is attractive, but Vietnam and Bangladesh are very attractive in terms of foreign investors, but even with this only 0.2% change is coming to India.

Ruchir Sharma: Yes, so both are looking at one, which is that it should be a lot higher, but two, the fact that there is this opportunity out there that people still want to outsource, that's the message, just not to China, and India has the scale if it can attract some of that also.

NDTV: So, the solution to this is that India must try to get that outsourcing that is moving out of China and going to India; otherwise, we must work harder. I mean, when I first started The World This Week, I mean the China change in wages when I was there before you were born, people were going around on bicycles with Mao outfits, thousands and thousands of bicycles on their main streets, I went into factories, they were Soviet type old fashion with poor everyone. Then came the first McDonalds, then came the first golf course and now there are two thousand McDonalds. Den Xao Ping I don't care whether a cat is black or white as long as it catches mice. So, we need to learn how to make things attractive, and they made things very attractive for foreign investment. How did they do that? What's the solution? How do we make ourselves more attractive for foreign investment?

Ruchir Sharma: It's multifaceted, you know, like the infrastructure you provide or the harassment you have or don't have from tax authorities or other people doing business in India, so I believe it's the entire ecosystem, not just one factor, that facilitates more foreign investment.

NDTV: This is a solution we really need to improve jobs and growth.

Ruchir Sharma: Yes, absolutely.

NDTV: To get this outsourcing that is currently going away from China, for a moment they come look at India and then go to Vietnam, so there is something we need to change and we need a solution on that. Your next point is that there will be a return to orthodoxy, and what do you mean by that? Just look at this, 10 developing countries with the biggest twin deficits, you mean fiscal plus external account deficit and India is in the top 10 of the World in terms of that, so this is a worry and now orthodoxy means change that.

Ruchir Sharma: No, in terms of the point I'm making here, which is that because the era of easy money is over, interest rates have risen everywhere, and financing in general has become much more difficult. In this environment, the scope for policymakers to do something too experimental, something away from what is defined as economic orthodoxy, which is that you need to follow a tight fiscal policy, you need to have relatively high interest rates, if you try do so something different the markets going to come and punish you. We saw that in the last year or so, exhibit A being UK where Liz Truss tried to do something too different in terms of cutting taxes and still not cutting spending and thinking she could blow the fiscal deficit out, the markets revolted and she in fact lost her job.

NDTV: So the world now looks very closely at deficits including your twin deficit?

Ruchir Sharma: So, the focus has come back when money is easy and there is too much abundance around. You could finance a lot of bad economics and bad behaviour.

NDTV: Unorthodox.

Ruchir Sharma: Unorthodox stuff like, so to speak, now that the scope is very limited, the question is for India, and it is the fact that we have generally followed an orthodox economic script that even though we have large deficits, we are not blowing them out, and one of the things for which I did sort of commend even the current folks for was that we did not over stimulate too much because there was so much pressure to do so.

NDTV: To over stimulate?

Ruchir Sharma: To stimulate and do that, and I believe you are aware that some countries, including Brazil, have done so, while others have paid a price for it, I believe it is critical.

NDTV: Back to orthodoxy, and to some extent, India has been reasonably orthodox in its fiscal and fiscal management. If you see India has actually been unpunished so far according to your data due to fiscal orthodoxy we've been careful India's fiscal balance has improved a little bit while the rest of the world in terms of emerging markets is got much worse or simply worse.

Ruchir Sharma: So what happened in the last year which is that these forecasts changed and India saw some improvements, so for now, even as I believe they present the budget, I believe the focus should be on orthodoxy and not any experimentation, because the temptation will be, with an election coming up in 2024, let's spend more, let's do more like stocks and stimulus

NDTV: In the run-up to elections, it's always like...

Ruchir Sharma: So you do not want the market to revolt against that because that would be a real problem?

NDTV: Very true What are they called? Are they ravedvi's? No, but again, as a section I would like to censor, you are saying you will have a relief from elections. We love elections. Why do you want a relief from them? Let's look at what your data says. 2023 unusually will be a light year for elections around the world, just before the elections storm in 2024; in 2023 no country has elections this year; this has not happened this century.

Ruchir Sharma: Among the G7 countries.

NDTV: Advanced yes, yes, yes.

Ruchir Sharma: In democracies, there isn't a single country that having elections in 2023, and that hasn't happened this century, so it's quite a coincidence that it's happened

NDTV: And you're saying in G20, the lowest number only two elections is the lowest in 35 years.

Ruchir Sharma: Yes, that is right.

NDTV: And that's what you are saying, but there are two elections, and the spotlight will be on possible regime change in Turkey and Nigeria. Are you saying this is based on opinion polls? Do you run a forecast? That's what people are talking about.

Ruchir Sharma: That's what people are talking about, the fact that there among the G-20 economies, which also include some emerging markets there are hardly any elections this year. So very rarely is something newsworthy for something not happening, and the fact that we have a bit of a pause in 2023 is very unusual as far as the global electoral cycle goes, but a couple of countries that are having elections that are not that big but still significant are Turkey and Nigeria and both those places if I can dare say so, that if you get a regime change it could end up being good for those countries, because in Turkey's case we are seeing Erdogan who started off strong has really run his economy into the ground. Now it's far from clear that he will lose but the opinion polls are pretty tight, so we'll see how that plays itself out so that election worth keeping on.

NDTV: And he's had one or two setbacks in local elections.

Ruchir Sharma: Yes, so I think that's an election worth keeping on, and also because there is so much fear about strong man rule and stuff in 2022 anyway; that was not a great year for strong men around the world, arguably, but we'll see what happens in 2023 in Turkey.

NDTV: And I just got your forecast for your travel in 2023; it is not going to be Turkey or Nigeria after these statements, is it?

Ruchir Sharma: It's always India for election travel.

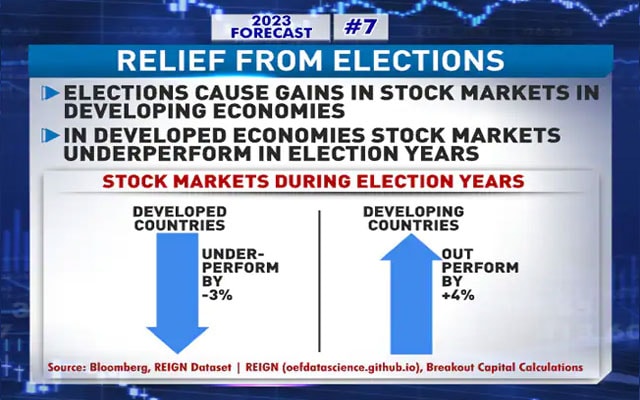

NDTV: No, no, I mean just for travel after you said, Well, the truth is okay. And; but elections are this amazing factor that you found that caused stock markets to gain in developing economies but in developed economies underperform in election years?" Look at stock markets during election years. Look at developed countries. They are down by 3%, underperforming relative to other stock markets. Developed countries, they overperform by 4%. Elections are good for developing countries' stock markets and economies, we should have lots more elections.

Ruchir Sharma: So this is a piece of research I had done earlier and we've spoken extensively about, which is that normally in emerging markets the best stock market returns tend to be when a new leader comes to power with a fresh mandate, because the new leader is most incentivized to carry out economic reforms.

NDTV: So there is hope?

Ruchir Sharma: So there is hope, and so when the potential for a leader to come in and change things is much more limited in developed countries, it leads to more volatility but not necessarily a better outcome, but in emerging markets, fresh leadership can often lead to better stock market performance, and that is something we may even see in Turkey and Nigeria, where with a regime change I believe the stock markets could fly in 2023.

NDTV: Now you're saying we should look out for Bluebirds when there's gloom and doom, when things are going well people look for black swans; we already knew that, but now we want to look for Bluebirds and the gloom that is being forecast, that you highlight here, is that not since surveys began, have forecasters thought that a recession is going to come, is more likely than it is now; the probability of a recession is the highest it has been for 50 years. Forecasters are now, of course, economists are invariably wrong, specially Bengali forecasters, but we do forecasts at least and we're wrong, but now a large, almost 50, over 40 percent are saying there will be a recession.

Ruchir Sharma: Yes, so the context here is this, one, as you point out that in the history of surveys, economists have never forecast a recession, so if a recession does happen in 2023, it will be the first time in the history of surveys that economists actually called a recession. But the broader point here is that generally, there is a lot of gloom around the world, and it's partly because of economics and partly because of politics because we've been through such a difficult period. There was the pandemic, and then there was the invasion of Ukraine, and then politics in many countries was not that favourable, with all sorts of surprise election results, and now black swans in general have become, rightly or wrongly, a symbol for what could go wrong.

NDTV: When things are going well, they tell you to be cautious of this or that, but when things are going badly, you look for Bluebirds, which I adore.

Ruchir Sharma: Yes, so I discovered that the Bluebird is a symbol of joy, of unexpected happiness, and thus it is a symbol of even hope. Even in the darkest of times, you should keep some hope that a Bluebird will arrive. So my point is that even though this is a difficult era and money has become much more difficult and interest rates are higher there is a lot of forecast about what will happen.

NDTV: It's going down in growth and inflation.

Ruchir Sharma: Growth while also being conditioned by all of Russia's shocks, such as the pandemic.

NDTV: In fact, you have a lovely list. In times of gloom, it may be best to look for Bluebirds rather than black swans, so it is bye-bye black swans. No one second, black swans are what we have just been through more in Ukraine with the terrible pandemic and Brexit having a huge impact on Europe and thus the rest of the world. We are looking for Bluebirds now, which you think may be Ukraine peace settlement, US-China reconciliation, maybe, and maybe inflation disappears. Look for them in this period of gloom.

Ruchir Sharma: Yes, because all of these are difficult to predict and are not the base case forecast, but my point is that in times of gloom, something unexpected may arrive and bring us joy, so the focus shifts to looking for Bluebirds.

NDTV: Ruchir, you had 97% last year; this year, you need to get 99.9%; can you run through your top trends for 2023 quickly?

Ruchir Sharma: Right, so I think the first one we discussed with the long grind that in the past we had V-shaped recoveries. Now we are likely to see a pattern that is more like a saucer shape or a smile in terms of that it takes a while for a downturn to set in but it takes a while for that to exit. The second one is a peak dollar, that the dollar had an amazing run over the last decade but it is now overdue for a correction, like has been the pattern for over 50, 60 years when it had such a strong performance and the fact that places like New York are the most expensive cities in the world tell you that the dollar is quite overvalued. Related to that is the fact that America also had a great decade but now, possibly beginning 2023 is bound to underperform the rest of the world because it's so overvalued and as a disproportionate share of the global stock market.

NDTV: And it's like a seesaw when they underperform and the rest of the world overperforms.

Ruchir Sharma: It's so large that, you know, we talk about the world, at least in replacement terms, as America and then the rest of the world. The 4th trend is about technology, which is that again, we are just coming off a big tech boom where too much money got thrown at too many bad ideas or a good idea gone too far funnelled by too much easy money. I think that's also coming to an end, and a lot of the big tech firms that did so well in that tech boom are likely to underperform in 2023. The 5th trend is that the same tech boom also lifted a lot of media companies because so much money was available for launching new streaming platforms...

NDTV: That should carry out. You are being censored here, okay. You are saying less money could mean better TV because quality checks will be much better.

Ruchir Sharma: Yes, and I think that could be true in India as well, that we will remember more of what we are seeing, and as we become more selective about content. The next trend I speak about is that Japan, nobody really cares about Japan; even our intellectual knowledge of Japan has atrophied by the fact it's been on the sideline for such a long period of time.

NDTV: High debt

Ruchir Sharma: High debt, bad demographics. But my point is that quietly, Japan may be beginning a comeback.

NDTV: Very interesting.

Ruchir Sharma: And related to that is the 7th trend, which is that labour costs in China have risen.

NDTV: Sorry, just one thing also. As you mentioned, with Japan coming back, that could help Indian investment in India a lot.

Ruchir Sharma: Yes, because Japan is a very key investment partner of India, and if Japan does well, it helps India, right? The 7th trend we discussed was on China, which is that people are still looking to outsource to countries such as America because the wages there are so much higher, but they don't want to do it to China anymore due to geopolitical reasons, and wages in China have gone up significantly, so therefore the outsourcing shifts to places in Asia including India, but we need to seize that opportunity, because so far it's the Vietnams of the world which have been the disproportionate beneficiaries of the outsourcing.

NDTV: So the solution to that is that India must be able to attract this investment better, because it is hardly attracting it now; it is going to Vietnam and other countries.

Ruchir Sharma: Yes, the 8th trend we discussed is the return of orthodoxy, and a common thread that runs through these trends is the return of higher interest rates, which means that you should be more careful in this environment.

NDTV: Don't be wild. Be more conservative.

Ruchir Sharma: That's right, don't you have done that orthodox; in India has done that so far and we hope that it's continued in the Budget and other policy announcements because the risk is always before an election year that if you decide to do too much but you don't want to do that kind of experimentation with other countries have suffered doing that, so far so good as far as India's concerned.

The 9th trend is about elections. That around the world it's quite an extraordinary coincidence that we just don't have too many elections this year taking place, national elections, and so the focus may be on some of the smaller elections, relatively smaller elections, like Turkey, Nigeria, but generally it's quite extraordinary where you have a year with no big election around the world.

NDTV: How will we manage without elections? But you did say that in developing countries, elections mean a boost to the economy and the stock market,

Ruchir Sharma: Especially when the leader changes.

NDTV: We miss the elections, so this is a relief.

Ruchir Sharma: That's what would happen. Nigeria, Turkey, yes, and the final one to summarise is that we are in a pretty gloomy environment given the forecast that most people have and how they are conditioned to negative shocks. So in this environment look out for what could be the positive surprises symbolised by Bluebirds that could come; we try to guess, but the very nature of surprises makes it impossible to forecast, so I believe that is where we are.

NDTV: That's the definition of a surprise. Well, you have certainly made some major forecasts, and they really will affect all of our viewers and our behaviour over the next year. Sometimes we do a mid-year one, but we will certainly do this again next year. And 99% or nothing, done?

Ruchir Sharma: That's not a very high bar. I'm not sure what to say in response.

NDTV: But only time will tell you.

Ruchir Sharma: Precisely.

NDTV: Yes, which is the worst cliche in the world. Well, thank you very much once again. We have once again learned a hell of a lot about that. Did I say that? I think that was misquoted, but no, I did learn a lot and I think everybody did. We will be following the economy with much more foundational knowledge based on all your data. Thank you very much and all of this is available on ndtv.com and Ruchir is also writing part of this for the Financial Times, so watch for this and watch for the new organization called Breakout Capital. I know you told me don't mention it but I have to. Thanks very much, see you again, bye-bye.

Here is the full transcript of the discussion:

NDTV: Hello and welcome to what I consider to be one of the most important shows that we've been doing for several years now and will continue to do so in the future. I must admit but don't tell Ruchir this, Ruchir how many years has it been?

Ruchir Sharma: It has nearly been a decade since we've done this show, but obviously we've been on television a lot longer.

NDTV: Right, I must admit and I was saying that I don't want Ruchir to hear this, that I learn more from this regular interaction with Ruchir Sharma than from almost any other programme that I've done. I must update you very quickly that Ruchir has now set up his own organization which is called Breakout Capital which is already doing brilliantly, has only recently started, so just watch this space.

Don't blush now Ruchir, I can see. I must point out like I do every year - all the research and analysis for this programme is done by Ruchir and his fantastic team and as you know it really is amazing research. Once again we should look at 10 major forecasts for this year, 2023. Let's first spend a few minutes understanding what actually happened last year and Ruchir your earlier forecast for 2022, shall we go through that - the 10 forecasts that you did get last year.

Ruchir Sharma: Yes, yes that's usually the routine.

NDTV: Okay, so let's look at the first forecast that Ruchir made in 2022 last year. Here it is. He said there'll be a decline in the birth rate and that will accelerate. In actual fact they didn't accelerate, birth rates stabilized a bit. There was a decline but they stabilized. The rate of decline in the world flattened a bit and India is also flattening a bit. Why that changed do you think?

Ruchir Sharma: You know I think what happened during the pandemic they got a major drop off in the birth rates of many people, but last year in 2022 in terms of the birth rates had been declining as you can see from the graph, the birth rates around the world have been declining dramatically really for the last few decades, and that pace has been accelerating in the last few years, did so even more during the pandemic. But in 2022 we saw a bit of a bounce back where the birth rates increased in some of the countries, possibly as a catch-up to what happened in 2020 and 2021. But the long-term trend I think still remains intact. Which is that the world is seeing a decline in the birth rates and therefore the population increases around the world have also being slowing down very sharply.

NDTV: And you pointed that related to a smaller workforce and that could affect growth rates of the economy.

Ruchir Sharma: Yes, and that's an affect that we are seeing around the world. Growth rates, the potential growth rate of the global economy due to declining birth rate and deteriorating demographics is falling everywhere. So the global economy which used to grow at let's say at 3.5, 4% now is lucky to grow at 2.5, 3% largely because of the demographic changes.

NDTV: I mean this is an amazing finding and I don't think many people, I don't think anybody else really related the two and then they just copied you. Let's look at the second forecast that Ruchir made last year. He said that China's economic power was peaking and actual fact, yes, China's economic power has peaked. if you look at the growth rate, look at it compared to the rest of the world, it was 10.3 compared to the rest of the world's 3.8. Back in 2000s about what, 7% above global, then it was about 5 to 4% above global and now China and the rest of the world's growth rates are about the same. So that rapid development compared to the rest of the world has seemed to have gone recently.

Ruchir Sharma: Yes so, that's my point, we are at that moment now where China, the best economic growth rates are well behind it, it is a middle-income country, it's facing all sorts of challenges. We spoke about demographics at the outset of the show. Very few developing countries have a demographic profile as bad as what China has because of its one child policy having such a lagged impact now. Its debt levels are very high. The property sector is really saddled with too much debt. And so therefore my forecast is also that in the coming decade China's growth rate is likely to be closer to 2.5% on average.

NDTV: That's a huge change.

Ruchir Sharma: Right and we only saw that in 2022 that China's growth rates fell a lot. Some of it I think was suppressed because of its zero Covid policy which had been a failure and now it's reversing course rather dramatically on that. So, China's growth rate might bounce back in 2023 but the long-term forecast based on demographics, debt and productivity is that China's economic growth rate is unlikely to be faster than that of the global economies. So, China's share in the global economy may have also peaked and that is a huge development because no country gained as much share in the global economy as China did in the last 4 decades. It was a dramatic rise.

NDTV: So dramatic I mean. As you showed growing at 10% on average for a few decades, it's just phenomenal and that's gone. I'm a bit surprised it hasn't gone up base effect because after the pandemic you think the next year there's a low base. The growth rate will be higher, but even that hasn't happened.

Ruchir Sharma: That may happen in 2023.

NDTV: Just because of the low base effect?

Ruchir Sharma: Yes because they were the last people to exit the zero Covid strategy, so that suppressed growth. So that may happen in 2023 but we're more interested what the long term trend growth rate in China is and I think it's two and a half percent a year, which means that it's unlikely to grow faster than the global economy for the foreseeable future.

NDTV: Ten percent to two and a half percent - that is just a phenomenal change. Let's move on to the next focus that Ruchir made last year. He said that the global debt trap will deepen, in actual fact, yes, mostly it did. But India was stable, the debt servicing cost of the share of income, if you look at the world, is rising, debt servicing rising India not rising, in fact falling a little bit if not stable. That's a big difference between India and the rest of the world.

Ruchir Sharma: Yes, this is mainly for the private sector, so I think that in India's case the private sector has the leverage. They have reduced the debt burden and so therefore they are in a better shape just now but around the world particularly in developed countries, in places like the US, they had taken on so much debt on the private sector side in terms of the firms, that as interest rates have gone up, the cost of servicing the debt has been going up a lot, so therefore the forecast last year that the debt gap deepens and it seems to have played out that way.

NDTV: Yes, that is a worry actually because implications for the future. Moving onto the next forecast that Ruchir made last year, this was that inflation will rise but may not hit double digits, that's quite a bold forecast and actually yes, it only increased to 8.8, it didn't hit double digits. Of course it did rise as Ruchir had forecast and it's kind of back to the levels of the 80's but didn't hit double digits, not terrible but still worrying because 8.8 is high.

Ruchir Sharma: I think a lot of people at the beginning of 2022 when we did this show were looking for inflation to rise. Some were looking for it to rise explosively. Others thought it would be transitory. I think we got something in the middle, that yes inflation did rise, but now it seems to have peaked, which is that across the world the inflation rates look to have peaked. But as we discuss in the show subsequently that it's likely to remain much higher than where it was in, let's say, in the 1990's or the 2000 so higher and stickier inflation but not the 1970s show where inflation was in double digits for a long period of time.

NDTV: Yes, that is a significant difference. The next forecast that Ruchir made last year was about greenflation that's about commodities and the commodity prices going up. He had forecast that global commodity prices in 2022 to remain relatively high, in fact commodity prices did remain high, in fact they went up fifteen percent. That is relatively high compared to other prices. Why is that still happening?

Ruchir Sharma: Yes that's a pretty significant outperformance because remember most assets like stocks and bonds around the world have fallen significantly in 2022. The reason that commodity prices have been more resilient has been because of oil, energy partly driven by what happened in Ukraine, but I think it's much deeper than that, which is that because of concerns about the green environment, you've had a lot of supply cuts, that not much new capacity is coming for commodities because people are very concerned about the impact it has on the environment and lots of regulations and political pressure is their dissuading people from...

NDTV: So, in a way there's a positive aspect of that - people are being more careful about how they mine, how they destroy the environment.

Ruchir Sharma: Yes but the negative effect is that fact that you are getting high commodity prices. So how do you get from point A to B remains a challenge. We all want to greener environment, but the problem is to build a greener environment it takes time A and 2 that it also requires some of the commodities to build the new green infrastructure, whether it's copper or aluminium, some of these so called dirty metals you need them to build the infrastructure.

NDTV: To improve the environment, it's a tough one ahead.

Ruchir Sharma: It's a tough one. But supply has been constrained and demand has been weak but because supplies been so constrained this time that even in a global slowdown, commodity prices had been relatively resilient led by the energy complex.

NDTV: Right. Moving onto the next forecast that Ruchir made last year and that was that productivity paradox persists, low productivity, there will be low productivity. Yes, in fact in actual practice, productivity remained low despite the tech boom. A lot of people said technology is going to change the world and you know productivity is going to go shooting up but we just see from his graph, that in 2021 there was a kind of post pandemic flare up because of unproductivity, partly because of the tech boom but then it's gone back again. There is low productivity now so the tech boom Ruchir has not improved productivity, it's a shocker.

Ruchir Sharma: Yes, there are many reasons for this. Some of the reasons that I've written about is that it could be that you have so many zombie companies out there, so many inefficient companies being artificially propped or were artificially propped by very low interest rates, too much stimulus, so that's been eating away at the creative destruction fabric of economy, so the explosion. And zombie companies, too much government intervention have been keeping many inefficient companies alive - that could be one reason for this.

The other reason, some people say, that the kind of technology we're seeing, whether it's gaming, or other things, are more distracting than enhancing as far as productivity is concerned. So I think this is a very deep research topic which is that why in the midst of the tech boom do productively numbers continue to look so poor. I think a good reason for that could be the fact that you have too many inefficient zombie companies which are kept alive. One statistic like in the US, the number of inefficient zombie companies, companies that are not able to even service their debt without borrowing more and more that, that number too shot up from nearly two percent in the 1980's to nearly twenty percent now.

NDTV: So 10 times, zombie companies have gone up ten times.

Ruchir Sharma: Yep that's right and that could be chipping away at the creative destruction fabric of any capitalist economy.